Sub-Saharan Africa’s gas production is estimated to grow by 18 per cent by 2021 to 9.1 bcf per day, said GlobalData, a leading data and analytics company with an extensive focus on Africa’s oil and gas industry

Nigerian National Petroleum Corporation (NNPC) will drive Sub-Saharan Africa’s gas production with 34.2 per cent share of all the production in 2021. Royal Dutch Shell Plc and Eni SpA follow with 10.4 and 7.8 per cent respectively, according to the oil and gas analytic.

In 2021, more than 6.4 bcf per day of natural gas will be produced by conventional gas projects, while coalbed methane (cbm) projects will contribute 8.5 mmcfd to Sub-Saharan Africa production in 2021.

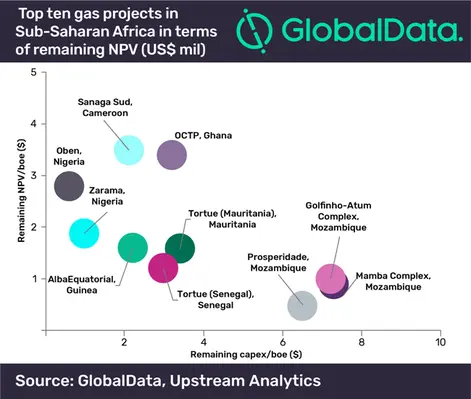

Speaking about Africa’s oil and gas analysis, Carlos Gomes, oil and gas analyst at GlobalData, said, “Sub-Saharan Africa has 28 key upcoming gas projects, of which, 16 will be producing by 2021. Empresa Nacional de Hidrocarbonetos EP and Eni SpA will lead in greenfield gas projects, with six projects each, followed by Exxon Mobil Corp with five projects in the near future.”

The region is considered to spend US$33bn as capital expenditure (capex) on conventional gas and CBM projects between 2018 and 2021, with spending peaking in 2021 at US$11.8bn. Average full cycle capex per boe for Sub-Saharan Africa gas projects is US$4.5. CBM projects have full-cycle capex of US$5.3 per boe, while conventional gas projects need US$4.5 per boe in full cycle capex.

GlobalData’s recent analytics in Africa’s oil and gas industry ranges from well-site and pipeline issues to upstream, midstream and downstream. In its analysis of global planned isomerisation capacity of refineries, GlobalData shows that Nigeria contributes 15 per cent of global isomerisation capacity, with China having the highest capacity globally.

“Deepwater projects have the highest average full cycle capex of US$7 per boe, followed by shallow-water, ultra-deepwater and onshore projects with an average full cycle capex per boe of US$5.4, US$5 and US$2.7 respectively.

New gas projects average $5.1 per boe in capex and need a gas price of US$6 per mcf to break even over the development timeline. Average development break-even price for planned and announced ultra-deepwater projects in Sub-Saharan Africa is US$6.4 per mcf, while the shallow water and deepwater projects have a development break-even price of US$6.9 and US$5 per mcf respectively. Onshore projects require a gas price of US$3.9 per mcf to break even.