Many international oil and gas companies (IOCs) are holding on to vast unsanctioned reserves in sub-Saharan Africa, along with large numbers of discoveries with no semblance of associated development plans, according to GlobalData, a leading data and analytics company

With strategies leaning towards a lower carbon future and a shift away from high-risk investments, resources that no longer fit this narrative risk being left behind by the IOCs currently holding them.

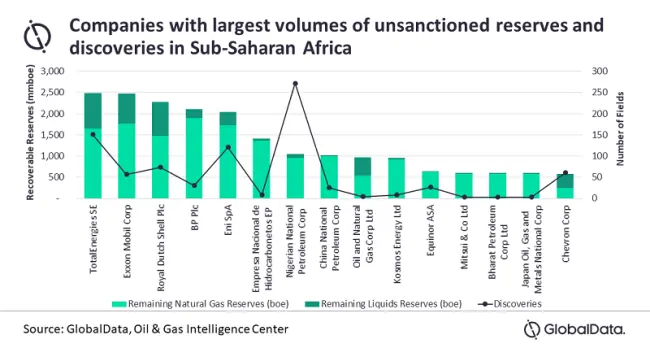

Conor Ward, oil and gas analyst at GlobalData, commented, “The top five companies in the region with the largest volumes of unsanctioned reserves are all major IOCs, with TotalEnergies sitting at the top of the pack and four out of five being European IOCs.

“Much of TotalEnergies’ unsanctioned reserves in the region come from the Prosperidade gas/ condensate development (discovered over 10 years ago) in Mozambique where final investment decision (FID) has been delayed many times already. Moreover, in light of market conditions and huge additional LNG volumes coming from Qatar in the near future, the prospects of Prosperidade coming online any time soon are looking unlikely. The company also holds significant resources in Kenya and deep-water Angola, which may no longer align with the company’s emissions strategy.”

Ward continued, “Over 80% of the unsanctioned reserves in projects across the region come from natural gas. Historically the resource was considered to be uneconomic in the region; however, the growth of LNG demand and LNG export infrastructure in sub-Saharan Africa provides opportunity for commercialising gas in the region.

“Despite gases longer-term potential, commercialisation is still challenged due to limited domestic demand, above ground risks and lack of export infrastructure. These factors, coupled with a market which is inundated with new volumes from elsewhere, mean that the sub-Saharan African projects continually face delay.”

These discoveries still represent an opportunity for joint/ clustered developments. For instance, a potential merger opportunity of upstream operations between Eni and BP in Angola would streamline operations. Therefore, such smaller developments are more likely to go ahead. Eni has had success of late with the Agogo and Cuica discoveries and fast-tracked production from both fields within nine months; this type of infrastructure-led exploration could be key to unlocking further resources.

Ward concluded, “Much of the resources held by the European majors are high risk and, in many cases, have marginal economics. Questions remain whether these resources will continue to fit into the emerging strategy of sustainability and emissions reduction. In the case that these assets no longer align with company strategy, there could be swathes of impairments to come.”